Many years ago, I asked my now nearly 90-year-old grandmother when the wisdom of age sets in and we start to feel in control of our lives. She made one of those “Ha!” noises and said she still felt like she was in her 20s, couldn’t figure out how she got to this point in her life, and would let me know when she thought she was in control. I’m still waiting.

Now that I’m firmly ensconced in middle age, I’ve started to understand a few things: why people have face-lifts and the importance of calcium. I’ve also sharpened my perception of what it means to control one’s life and our power as individuals within an economy. Unfortunately, the design and assumptions used in our modeling of the economy attempt to minimize individuals’ impact and importance, but you can do something about that.

Why You Lost Control of the Economy

First, a little background. The artificial distinction between microeconomics (concerned with individuals, households, and businesses) and macroeconomics (concerned with the economy as a whole, including unemployment, inflation, and GDP) in the discussion of the economy came about when John Maynard Keynes wrote The General Theory of Employment, Interest, and Money. One of the problems economics had was that it was considered a “soft” science due to its inability to model and predict behavior in the economy like the “hard” sciences such as physics and chemistry. After all, people are complicated. How can we possibly expect what decisions they’ll make in the economy?

To move the study of the economy closer to the hard sciences, Keynes had to remove those things that make us human values, motivations, ingenuity, and potential reports on and attempt to manipulate (through monetary and fiscal policy) the economy’s condition as a whole. Individuals’ rationality within his model is assumed to be inherent, and individuals are believed to have all the information required to make optimal decisions, have not learned from previous experiences, and are not influenced by other people. Even Adam Smith’s “rational choice” theory recognized the influence on the economy of “moral sentiments.”

The result has been that we, as individuals, have been stuck within a closed system to explore the economy that doesn’t consider our roles. This secure system assumes we have a uniform set of values, and our personal lives and relationships are irrelevant to the overall design. We cannot influence the economy or its structure. There is no mechanism to measure individuals’ economic impact when utilizing a Keynesian macroeconomic approach. As a result, we have come to rely on governments to fix our financial woes rather than attempting to tackle them ourselves. We have forgotten that macroeconomic data is the sum of all particular economic activity.

How You Can Help the Economy

Since macroeconomic data is the sum of individual activity, you CAN impact the economy; your actions DO matter. So stop worrying about macroeconomic “facts,” like unemployment rates, designed to bring the study of the economy closer to the hard sciences, start thinking about your probabilities and possibilities, and then get busy.

Here are a couple of things you can do to impact macroeconomic data for the economy. First, consider the possibility of having a million dollars when you retire. It’s more obtainable than you think. If you make $35,000 a year, get annual pay increases of about 3.5%, and save around 12.5% in a 401(k) over a 40-year career, you could have a million dollars (assuming a 7% return). Remember that your employer might kick in some of that 12.5%, so that burden is not entirely on you. Even if you did have to save it all, we’re talking about $84 a week (which, after taxes, is less) to ensure you have retirement money.

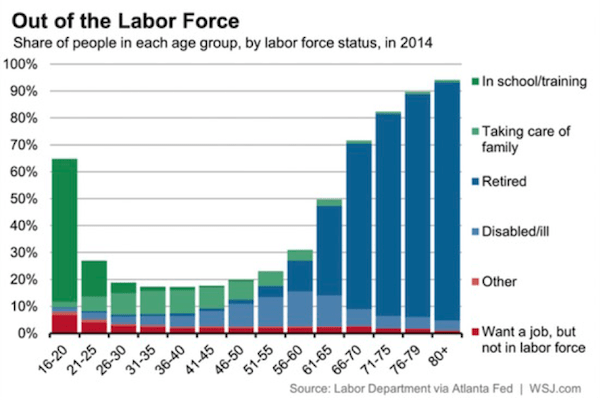

How does this help the macroeconomy? For one thing, the current average retirement savings is $60,000. Let’s say you don’t get as many pay raises or earn a 7% return, and you end up with only $800,000 or $500,000. You’re still helping to increase average retirement savings. More retirement savings by more people means fewer problems for the macroeconomy later. Even though a million dollars is obtainable even on a modest income, only 0.2% of people reach that goal. The problem? Too few individuals understand their real power in the economy and fail to see the possibility of improving themselvesff. Instead, they rely on the government to come up with a solution. These people aren’t stupid; they believe they are powerless and at the macroeconomic environment’s mercy. Thank you, Keynes.

{kind=link}